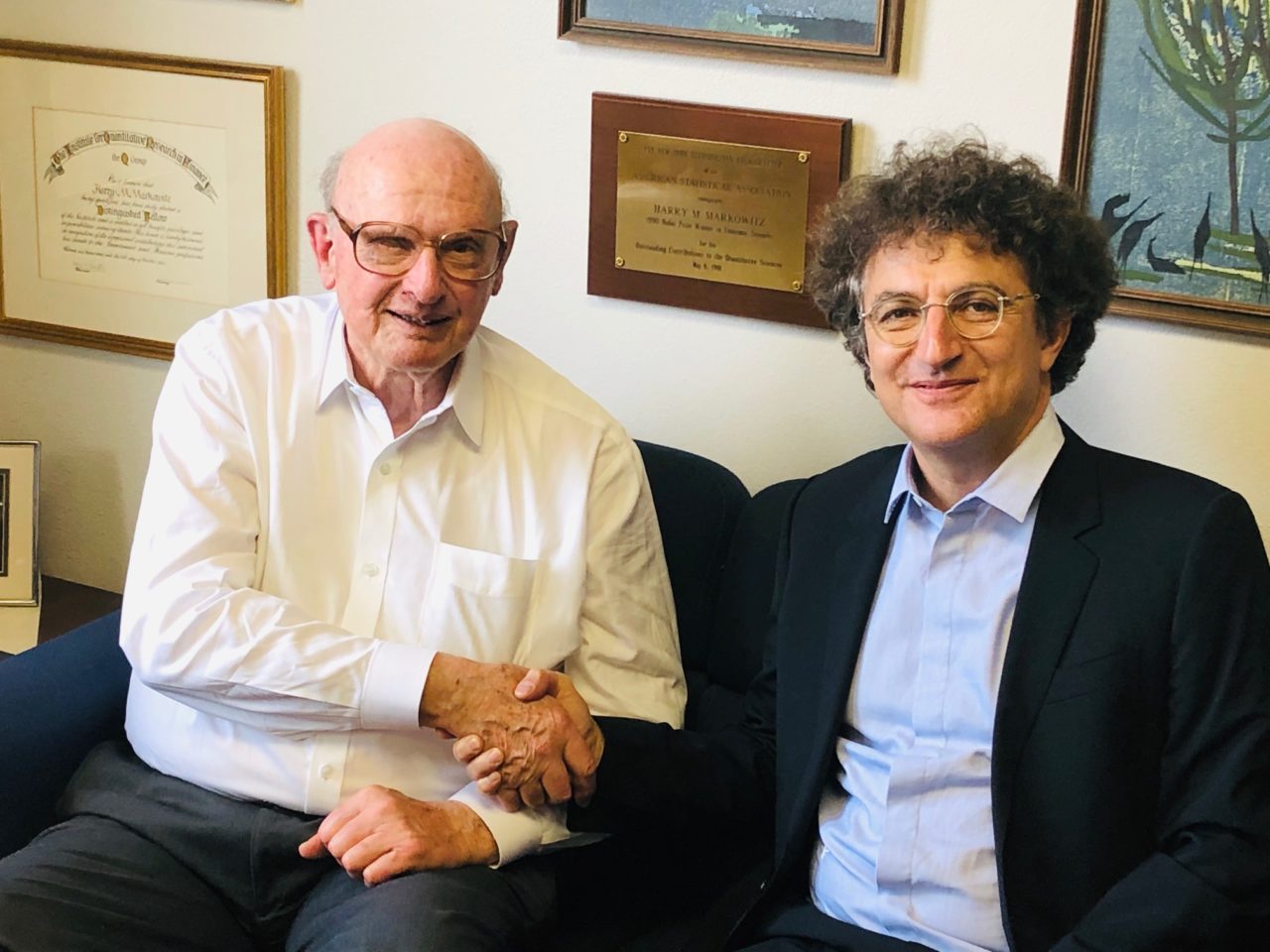

Harry Markowitz by Yves Choueifaty

The afternoons of june 10th and 11th 2019 were amongst the most exciting times I have ever had in my professional life.

This was the second sentence that Harry Markowitz said when welcoming me in June 2019 into his office in San Diego before inviting me to explore his library.

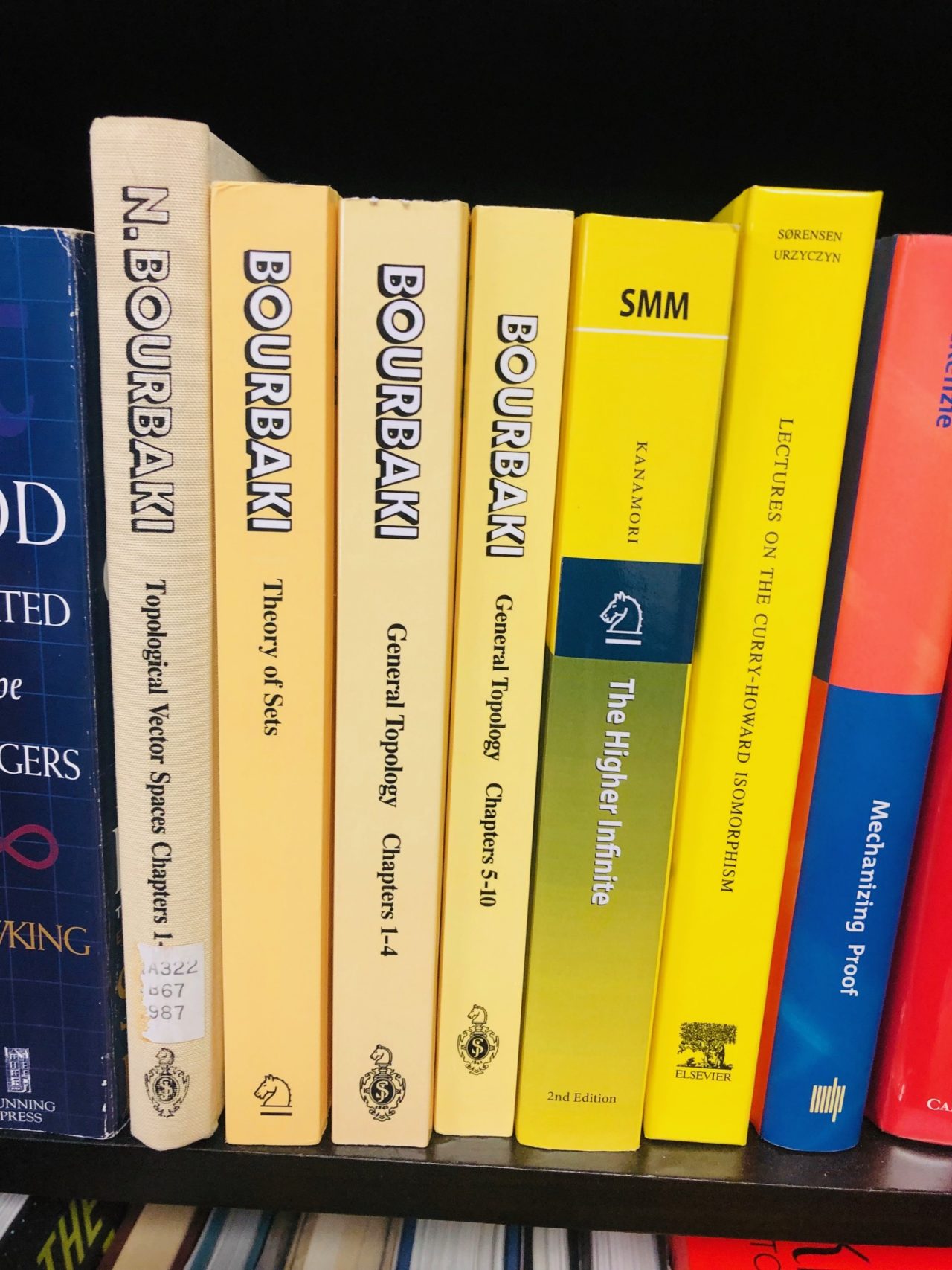

“I am what I read”, said 92-year old Harry Markowitz, in front of his extensive library. Some were economic books as one could expect from a winner of the Nobel Prize in economics. However, it is a very diverse and organized collection, with an important allocation to History and Mathematics. If his library defines who he really is, Harry Markowitz is definitely a well-organized mathematician and philosopher.

We were delighted to find in his library the works of Nicolas Bourbaki, the collective pseudonym of a French school of mathematics that aimed at reformulating mathematics from the ground up, in a self-sufficient, formal and rigorous way. We should not have been surprised, as Markowitz’s framework is derived from the economics of uncertainty, starting with very basic formulations of preferences towards risk.

The “Bourbaki spirit”, one of tobam’s founding values, means that we aim to avoid using conventional wisdom when it uses unclear definitions.

I also have established a now decade-old tradition at tobam to offer each of the new employees, after a certain period with us, a book entitled “Gödel’s Proof”. Harry’s first shelf contains the works of my four favorite mathematicians: Bourbaki, Euclid, Gödel and Cantor, whose triadic set I often quote when in need to give an example of counter intuitive results.

I have always been proud to proclaim that TOBAM’s approach to investment walks in the footsteps of the ground-breaking work undertaken by Harry Markowitz almost 70 years ago.

Harry Markowitz looks at the merit of a portfolio for what it brings to its owner in terms of return and of risk rather than as a result of an equilibrium which can be argued is based under a set of fallacious assumptions.

Echoing what Harry said, it indeed strikes me that sometimes the most obvious is not always defined and deconstructed.

And indeed, a central result of Modern Portfolio Theory is that ‘diversification is the only free lunch’, in the words of Harry Markowitz.

Harry’s revolutionary approach was to recognise that the standard deviation of the returns of a portfolio of equities, or assets in general, will be reduced by the extent that the securities are uncorrelated with each other. Combining stocks which tend to move in different directions will reduce the overall portfolio standard deviation to levels below that of individual stocks. It is then possible to produce an “efficient frontier” of portfolios, each of which maximises future return expectations for a given level of overall portfolio risk. That insight, which seems so obvious today, was a revelation when it was first put forward.

The mathematical problem that Harry Markowitz solved was that, given a set of stocks and their expected returns, standard deviations and correlations among each other, how do you determine the set of portfolios that maximizes the expected return for a given level of risk? He devised an algorithm in 1956 known as the ‘critical line algorithm’ which produced a set of “efficient” portfolios that maximised returns for a given level of risk, tracing the now famous “efficient frontier”.

What TOBAM does can be seen as an extension of this very idea in the case when we have no a priori views of the expected returns on individual stocks. Our objective is then much simpler than trying to produce an efficient frontier of risk and return as we don’t need to come up with expected returns on each investment but instead, just end up maximising diversification. In this case, you have to formulate a neutral assumption based on the fact that, when arbitraged, the prices are organized in a way that future risk contributions are perceived to be equal. tobam’s Diversification Ratio® is the function that needs to be maximised in order to ensure that the marginal contribution of any stock in the portfolio to the total portfolio risk is identical.

Since Harry Markowitz’s ground-breaking work, a whole new field, known as “financial economics”, has arisen and numerous papers on exploring and developing further insights are published each year. However, it is fair to say that Harry Markowitz’s original approach has stood the test of time and is the benchmark of what a well-constructed approach to investment could be.

Harry was initially looking at the problem of risk and return in a portfolio of equities, although clearly the theory has general validity for a portfolio of any number of asset classes as well as individual components within an asset class. The calculation of efficient portfolios using the critical line algorithm requires quite complex mathematical manipulation involving inversions of matrices representing the securities being looked at. Analysing a complete stock market of one thousand or so securities would require an inversion of matrices consisting of a thousand rows and a thousand columns and calculations of correlations of one stock with each and every one of the other 999. Such calculations were not economically feasible using the computing power available for decades after Harry’s work first came out. That may have provided the spur to further theoretical developments in the form of the single index model developed by Bill Sharpe, which essentially simplifies the problem of trying to assess correlations of one stock with hundreds of others, by giving an approximation: namely that a large amount of the behaviour can be explained by the correlation of the behaviour of one stock with the average of all the other stocks, that is with the market index. This approach led on to the ideas of the Capital Asset Pricing Model and subsequently, to the ideas of efficient markets.

Having the opportunity to discuss tobam’s approach to risk diversification during two consecutive afternoons with the father of Modern Portfolio Theory in Sunny San Diego, was a very moving experience for me. Our philosophies are so close that whilst Harry is well known as the father of Modern Portfolio Theory, I can now confirm even more strongly that Harry is truly the godfather to tobam’s investment philosophy.

In 1990, the Royal Swedish Academy of Sciences awarded the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel to, among others, Harry Markowitz for his role in the foundation of Modern Portfolio Theory (MPT). 30 years later, and more than 60 years after the original papers, are Markowitz’s insights still relevant for the finance practitioners?

We, at TOBAM, believe they are. They indeed directly inspired our management philosophy, and we recently embraced the opportunity of meeting him.

TOBAM offers a quantitative management approach which integrates socially responsible investment criteria via an exclusion list.

Applied to equity and fixed income strategies, respectively since 2007 and 2015, we are looking at Maximum Diversification® indices since 2011, this negative screening is based on the exclusion list published by the Norges Bank, a renowned investment institution and founding member of the PRI , as some other leading institutions.

This exclusion list involves controversial products ( Tobacco, Coal, Weapons ) and other controversial behaviors ( Human rights, Environment and International Laws, severe damages or breaches ).

We are committed to third parties, the industry and the investment companies as another crucial step towards the promotion and development of responsible investment.

TOBAM also applies a 100% fossil-fuel free approach to two of its strategies: Anti-Benchmark® Emerging Markets Equity and Anti-Benchmark® Global High Yield.

Companies with significant involvement in the production, sales or extraction of fossil fuels (including coal, coal power generation, oil and gas) are excluded from the investment universes of both strategies.

Downloads :

Your jurisdiction may not give you full access to the list of funds distributed by TOBAM, for more information please contact [email protected]

[ivory-search id=”255063″ title=”Default Search Form”]

US PATENT

CANADIAN PATENT

AUSTRALIAN PATENT

JAPANESE PATENT

The Client Service & Business Development team coordinates Client Service and Business Development from Paris and New York offices, and has been continuously expanding together with TOBAM’s AUM growth. The team evolves in a multicultural environment and currently includes members from Europe, America, and Asia.

The Client Service & Business Development team in Paris sits together with the Portfolio Management and Research Team which facilitates the cooperation and constant flow of information between the different teams.

Job Description

The Candidate prerequisite

Please send over your ENGLISH CV.

Contact

Job Description

The candidate will:

The Candidate prerequisite

Definite plus: Strong Academic track record.

TOBAM, a quantitative asset management firm with assets approx. $10 billion and 51 professionals (as of December 2021), is currently recruiting an intern to join its Paris-based Client Service & Business Development team. The company offers innovative investment capabilities and provides institutional clients with diversified core equity exposure, both globally and in domestic markets. The firm has been experiencing a significant expansion, one of the largest in the industry, and is looking for a candidate who can contribute to its strong growth.

The Client Service & Business Development Team

The Client Service & Business Development team coordinates Client Service and Business Development from Paris and New York offices and has been continuously expanding together with TOBAM’s AUM. The team evolves in a multicultural environment and currently includes members from Europe, America, and Asia.

The Client Service & Business Development team in Paris sits together with the Portfolio Management and Research Team which facilitates the cooperation and constant flow of information between the different teams.

Job Description

The Candidate

Top-notch business or engineering school.

English fluency and strong writing skills are required.

Strong computer skills : advanced in Excel,

Strong analytical skills, team spirit, proactive, attention to detail, keen to learn and learn fast.

Please send over your ENGLISH CV.

Contact

Born in Bayonne (South West of France) in 2001, Justin grew up with his feet in the sands.

Supported by his parents who 15 years ago, established the Natural Surf Lodge, between lake, forest and ocean. This environmentally responsible living environment, provides Justin with a beneficial and suitable structure for his training.

A native from the European capital of board sports, Justin has a great desire to travel the world (Australia, Tahiti, Hawaï, Denmark..) which he will be able to do upon being successful in joining the professional circuit, the CT.

In 2022, Justin has been selected to join the highly prestigious Rip Curl Pro Portugal event and is looking to participate to the Olympic games in Paris in 2024.

TOBAM is proud to support this young athlete, who remains humble and accessible. Go for it Justin!

If you want to learn more about Justin, please read “Life of a Surfer“

We are really proud to have another beneficiary of the Initiative, Aurélia Boulanger, a very talented young triathlete.

Aurelia just graduated as an engineer, specialized in urban planning and sustainable buildings.

She started her triathlete career in 2018, and became the winner of the 2019 French long distance triathlon.

TOBAM is proud to support a female athlete, in a sport that is less prone to media attention but requires an absolute dedication and commitment to trainings and competition.

Her objective this year is to qualify for the Triathlon 70.3 World Championship, due to be held on December 2022 in New Zealand. This “half-Ironman” is a long-distance triathlon race consisting of 1.9km swim (1.2 mile), 90km bike (56 miles), and 21.1km run (13.1 miles) !

Aurelia’s dedication to her sport, trainings and objectives sets a high example for all of us. We are happy to support Aurélia for her future endeavours.

Discover Aurélia’s interview from April 2022

Good Luck Aurélia!

Since the adoption of Norges Bank’s exclusion list in 2007, tobam has implemented a number of initiatives to further supplement its sustainable investment approach. tobam’s research department dedicates a significant amount of its time and resources to study the ways in which sustainable investment and ESG topics can be integrated into portfolios without disrupting tobam’s Maximum Diversification® philosophy.

tobam’s research team carried out extensive research on the reduction of the carbon footprint of our portfolios via the implementation of a carbon footprint constraint compared to the market cap weighted benchmark of the investment universe.

Based on our findings, we demonstrated that a systematic reduction of 20% of all of tobam’s portfolios carbon footprint versus their respective benchmark has no significant impact on the portfolio’s risk/return profile, nor on its diversification benefits.

This relative carbon footprint reduction constraint was implemented in the portfolio optimization process, for all Anti-Benchmark® equity portfolios since June 2018, to all Maximum Diversification® Indices since September 2018 and to fixed income portfolios since June 2019.

TOBAM considers stewardship as a way to consider its shareholder and creditor position on behalf of its clients to influence investee companies, investors, the asset management industry and our clients. The objective is to take responsibility for long-term value creation, including the value of common economic, social and environmental assets.

TOBAM uses several tools to achieve an efficient stewardship policy and further integration of sustainability principles and good corporate governance in the companies in which it invests.

TOBAM’s Stewardship policy’s primary objective is to identify and influence investee companies under controversies or facing long term challenges and to use our shareholder and creditor responsibility as a way to further the dialogue and to influence best practices. Management of potential reputational, legal, environmental, social risks is the priority of TOBAM’s stewardship policy.

TOBAM uses General Assembly Votes, Engagement, Contribution to Public Goods (Research) and Public Discourse (media & Conferences) to enhance its stewardship responsibility, reach better understanding of investee companies’ policies, develop risk monitoring of controversies, sustainability and climate related risks and promote best practices.

Downloads :

| STEWARDSHIP POLICY | ENGAGEMENT POLICY | VOTING REPORT | ALL VOTING DECISIONS | ENGAGEMENT REPORT |

TOBAM’s Research team has built a proprietary methodology to construct the Sustainability Performance Footprint of each individual stock holding in our portfolios, hence the sustainability performance footprint of our portfolios.

Using officially published data from Bloomberg in order to monitor the sustainability criteria for all listed companies of our investment universe:

TOBAM’s is now integrating sustainability and has implemented this hard constraint to all our equity portfolio, in order to optimize portfolios so that they, at minima, match the footprint of their respective benchmark.

As usual, TOBAM’s integration efforts is built in parallel to significant research efforts to ensure that these new additions did not significantly impact the characteristics of our portfolio in terms of risk/return profile, as well as diversification structure.

TOBAM is currently working on integrating the sustainability performance footprint to fixed income portfolios.

Downloads :

| SUSTAINABILITY REPORT | SRI POLICY | ADVERSE SUSTAINABILITY IMPACTS STATEMENT |